Navigating the Road Ahead

Australian Property Investments Advocacy is always paying attention to the trends and movements of the country’s real estate market. We do our due diligence in researching key factors and using the data we find to help you make smart investment decisions.

What’s Next for the Australian Property Market

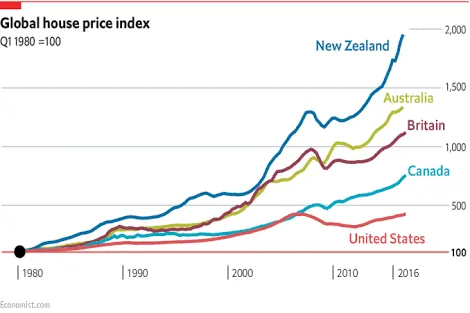

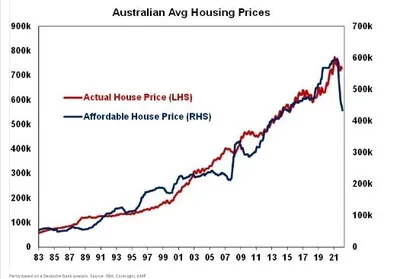

The country has experienced incredible capital growth in recent years, with many areas still providing value. There are many reasons for this, but one of the main culprits is property investment both foreign and local. With property tax-efficient schemes, government incentives, and cheap financing, property investing has become a second income for many.

In mid-2022, housing prices increased by double digits in five of Australia's eight capital cities. Property prices are expected to rise over the long term but not everywhere. Knowing where to invest and when, will be key to maintaining portfolio growth.

Financing rates are less attractive now (and some trepidation still exists), however, the restricted supply and the positive consequences of population growth will lead to another mini-housing boom in 2023–2024.

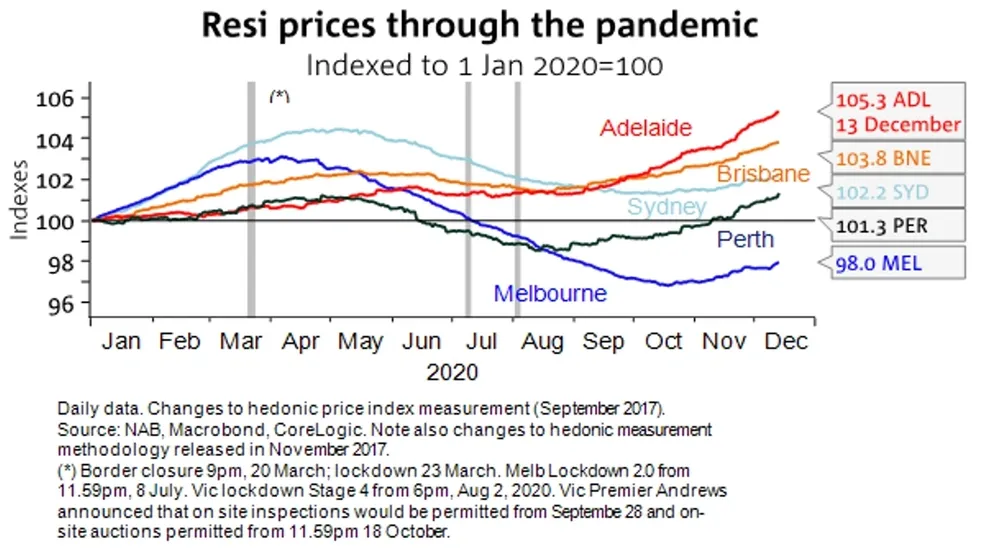

While Sydney and Melbourne lost some of their gains in 2022, we still expect home prices in these cities and several others to climb consistently in the years to come. Adelaide and Brisbane look set to boom again.

Our Key Predictions for 2023-24

House prices to rise by 3-5% in Perth, Darwin, and Hobart

House prices to rise by 5-8% in Canberra, Brisbane, and Adelaide

House prices to rise by 1-3% in Melbourne and Sydney (area dependent)

Apartments prices to rise by 5-10% and will rebound strongly in every major city

Why Invest in Australian Properties

You can start investing in Australian real estate with very little initial cash. More importantly, the rental yield is still positive in many regions. This means these investments can naturally pay down their debt over time while realizing capital gains.

Both of these factors make Australian properties solid nest eggs or pension income sources.

")

The Aus Property Investments Blog

What is Negative Gearing?

By Australian Property Investments Advocacy |

How to Create a 5 year Investment Plan

By Australian Property Investments Advocacy |

How to use your Super to buy a house

By Australian Property Investments Advocacy |

What it costs to buy a home with only a 10% Deposit?

By Australian Property Investments Advocacy |

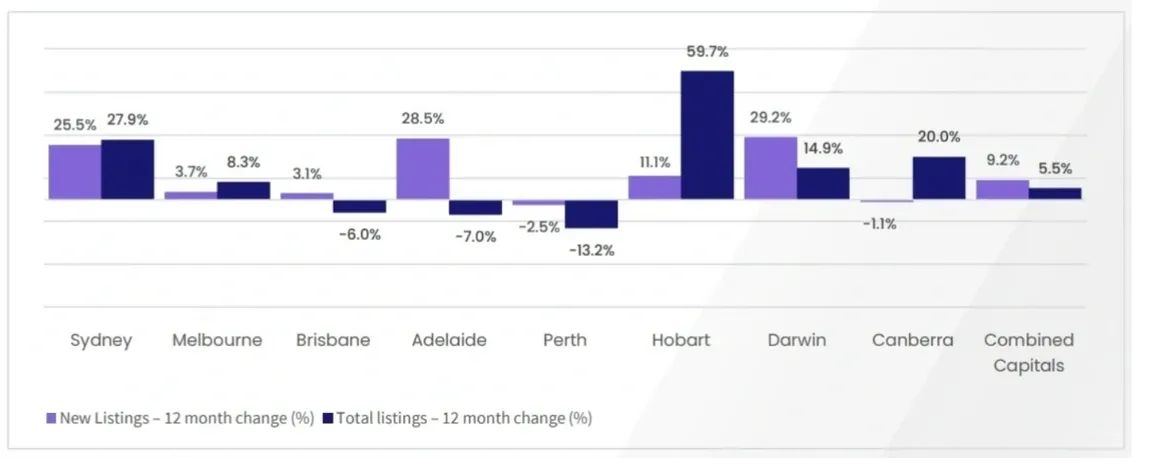

Property Price Performance